Decision-Making Under Uncertainty (2/3) || Why I Optimise For Probability, Not Returns

How relaxing precision, time pressure, and false certainty changed how I invest

This article is part of the Zenca series Decision-Making Under Uncertainty, which explores how to make better financial choices when outcomes cannot be predicted.

In the previous piece, I argued that markets force trade-offs - whether we acknowledge them or not.

High returns, short timelines, and low risk cannot coexist with certainty.

Something always has to give.

This article is the second in the Zenca series Decision-Making Under Uncertainty.

Here, I’m not making a universal recommendation.

I’m simply explaining the trade-offs I choose to live with, and why I optimise for probability of success rather than returns.

For a long time, I framed investing the way most people do.

I asked questions like:

What returns should I expect?

Is this good enough?

Can I do better?

That framing is so common that it feels natural. Sensible, even.

Over time, I realised something uncomfortable:

returns were never the thing I was actually trying to optimise.

They were the story I told myself about progress.

The real objective was something else entirely.

Probability.

Returns were never the objective

Returns are an outcome.

They are what fall out at the end of a process - sometimes generously, sometimes disappointingly, sometimes randomly.

Yet we treat them as if they are something we can directly aim at.

When I stopped doing that, my entire approach changed.

Instead of asking “How much can I make?”

I started asking “How likely is it that this works?”

That question is quieter.

Less exciting.

Much harder to market.

But it is far more honest.

Why certainty about returns is a false comfort

At some point, I noticed a pattern in my own thinking.

I would mentally anchor to a number - 12%, 15%, 20% - and treat it as a baseline expectation.

Not a guarantee, but something like “at least this much.”

That expectation did nothing useful.

It didn’t change the future.

It didn’t make markets cooperate.

It didn’t reduce uncertainty.

All it did was create a reference point - one that reality was almost guaranteed to violate at some point.

There is no way to know returns in advance unless you deliberately choose fixed income.

Anything else is estimation, storytelling, or hope dressed up as precision.

Me expecting “at least 18%” doesn’t increase the odds of getting 18%.

It just sets me up for disappointment when the path doesn’t cooperate.

Once I accepted that, I stopped demanding certainty from something that cannot offer it.

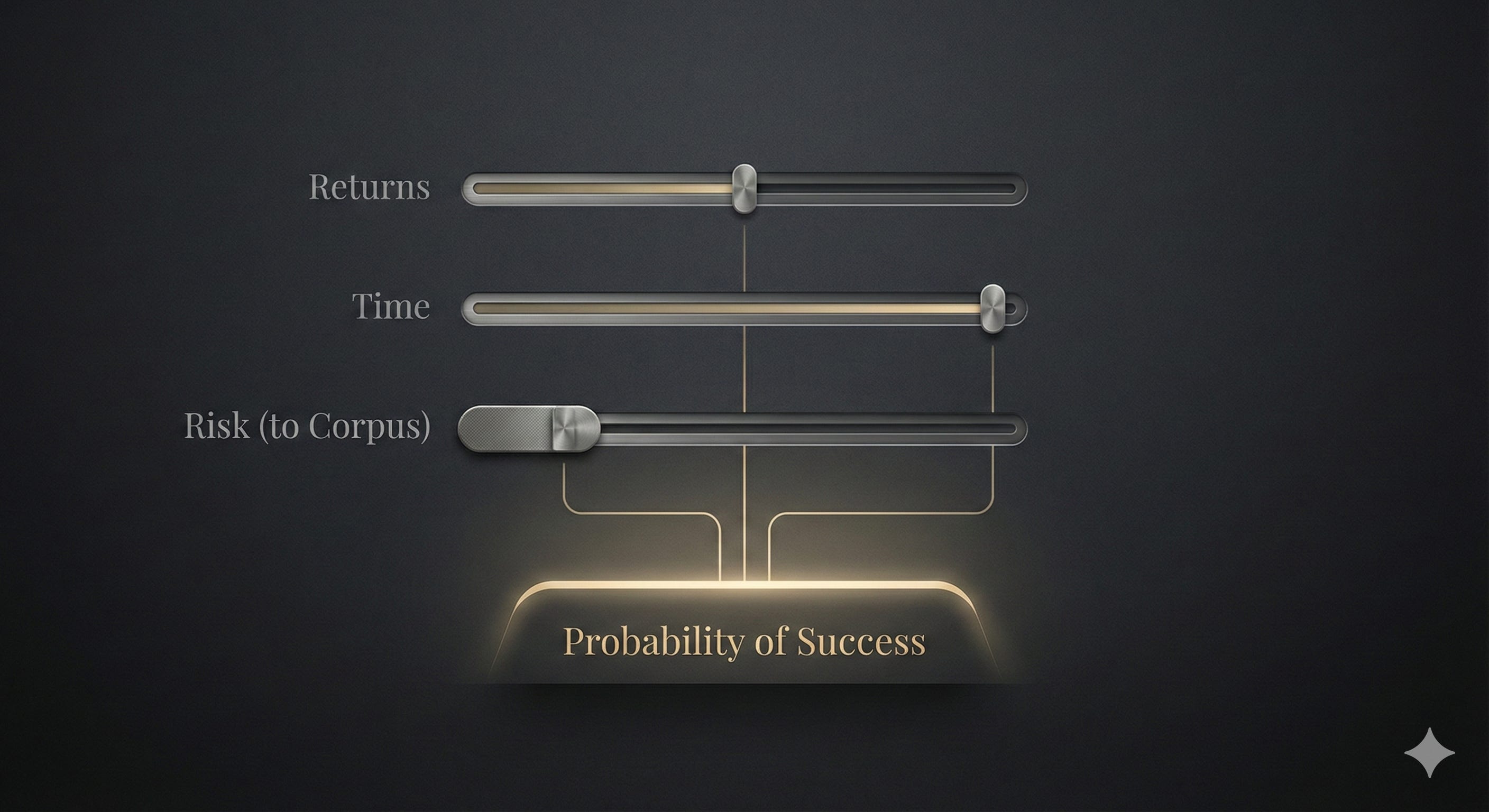

The levers I consciously adjusted

Once probability became the objective, the question shifted.

If I can’t control outcomes, what can I control?

The answer wasn’t complicated.

It was uncomfortable.

Returns - what I stopped demanding

I stopped anchoring to a return number.

Not because returns don’t matter - they do - but because demanding them in advance is meaningless.

Returns will be what they will be.

Wanting them harder doesn’t make them arrive faster.

Naming them more confidently doesn’t make them more likely.

Letting go of return precision didn’t lower my ambition.

It removed a false sense of control.

Time - the lever that changed everything

Time was the most powerful adjustment.

I relaxed my time horizon.

I stopped forcing outcomes into neat windows - 5 years, 7 years, 10 years - simply because those numbers felt reasonable.

Time absorbs volatility.

Time absorbs mistakes.

Time absorbs bad luck.

Short timelines turn noise into risk.

Longer timelines allow noise to remain noise.

The moment I stopped asking “Will this work by X?”, probability quietly improved.

Risk - what I refuse to compromise on

Here, I use “risk” in the same sense as before: risk to corpus.

Risk is not volatility.

Risk is the possibility of permanent impairment of capital.

This is the one lever I am not willing to relax.

Once capital is impaired permanently, probability doesn’t decline linearly - it collapses.

Recovery takes longer, options narrow, and flexibility disappears.

This non-linearity is not abstract.

If you lose 20% of capital, you don’t need 20% to recover. You need 25%.

If you lose 25%, you need 33%.

If you lose 50%, you need 100%.

Losses shrink the base on which future returns compound.

The deeper the loss, the steeper the recovery required.

This is why permanent impairment is so dangerous.

It doesn’t just reduce returns - it structurally lowers the odds of recovery.

Staying in the game matters more than upside.

This doesn’t mean avoiding drawdowns.

It means avoiding decisions that permanently damage the base on which everything else compounds.

Instrument selection - how I reduce risk without demanding certainty

As I relaxed my constraint on time, the one thing I sharpened was my choice of instrument.

My objective here is not to eliminate capital impairment altogether.

That becomes impossible the moment you move beyond risk-free returns.

My objective is narrower and more realistic:

to eliminate the risk of permanent capital impairment.

I am completely comfortable with temporary impairment of capital - drawdowns, volatility, long stretches of underperformance - as long as I believe I am riding the right asset.

Patience can heal temporary damage.

It cannot heal permanent loss.

This is why instruments like broad equity ETFs - and even Bitcoin - work for me.

Given an open-ended window of time, the likelihood of these assets leading to permanent capital loss is, in my assessment, zero or very close to zero.

That belief doesn’t come from optimism.

It comes from understanding what these assets represent:

productive economic systems, or monetary networks, that have no natural expiry date.

Why I stay away from instruments that require time precision

This same logic explains why I stay away from instruments that require me to be right about time.

I am reasonably confident that something like the NIFTY50 index (India’s benchmark equity index) will be higher over a long enough period, as the economy expands.

What I am not confident about is when it will hit any specific level.

The moment an instrument requires me to be right about both direction and timing, my probability of success collapses.

At that point, it doesn’t matter that a well-placed F&O (futures and options in India) trade can generate 100% returns in a month.

The odds of getting wiped out are simply too high - easily north of 90%.

For me, that is a trade that is not worth having.

No payoff is attractive enough to compensate for a near-certain probability of failure.

Why I don’t have time-based corpus targets

This part often surprises people.

I don’t have time-based targets for corpus size.

Not because I don’t care about outcomes - I do - but because time-based targets distort behaviour.

Firstly, no one can predict the future.

There are far too many variables, interlinked with each other in ways that are not only difficult to fathom, but impossible to model, for anyone to know that a certain annualized return outcome beyond the risk-free rate can be definitely achieved over another specific period of time.

Secondly, time-based targets create pressure where none is needed.

They force premature decisions.

They reduce flexibility precisely when flexibility matters most.

Targets can make sense in specific, constrained contexts.

But over long horizons, they often turn probability management into deadline management.

I would rather preserve optionality than optimise for a calendar milestone.

That trade-off is intentional.

What this optimisation gives me (that returns don’t)

Optimising for probability changes how investing feels.

There is less urgency.

Fewer forced actions.

Less reaction to noise.

Decisions become easier, not because the future is clearer, but because fewer things demand a response.

This isn’t about peace of mind.

It’s about consistency.

Consistency across cycles matters more than brilliance in one.

This is not universal

This is not the only valid approach.

Different lives require different trade-offs.

Some people need speed.

Some people need upside.

Some people are deliberately making bets.

There is nothing wrong with that - as long as the trade-offs are understood.

This is simply the combination I choose to live with.

What comes next

Once probability becomes the objective, a new question emerges naturally.

How do you structure your finances so that probability stays high when uncertainty persists longer than expected?

That question isn’t about predictions or precision.

It’s about structure.

In the next and final piece of this series, I’ll look at how asset allocation functions as a decision-making tool under uncertainty — not to maximise returns, but to avoid being forced into the wrong decisions at the wrong time.

Disclaimer

This is educational content, not financial, investment, tax, or legal advice.

Zenca shares perspectives and frameworks to help you think clearly - your decisions are your own.

Please think independently and do your own research.

I write to improve how we think about money.

If this helped you think more clearly about money, you can subscribe to Zenca to receive future essays directly.

Every subscription is a vote for thinking more clearly about money.

And if this resonated, take a few seconds to share it — it might change how someone else thinks about money too.