Inflation Reframed (2/5) || Why the Inflation Number Feels Wrong (Even When It Isn’t)

CPI measures how inflation shows up - not why it exists.

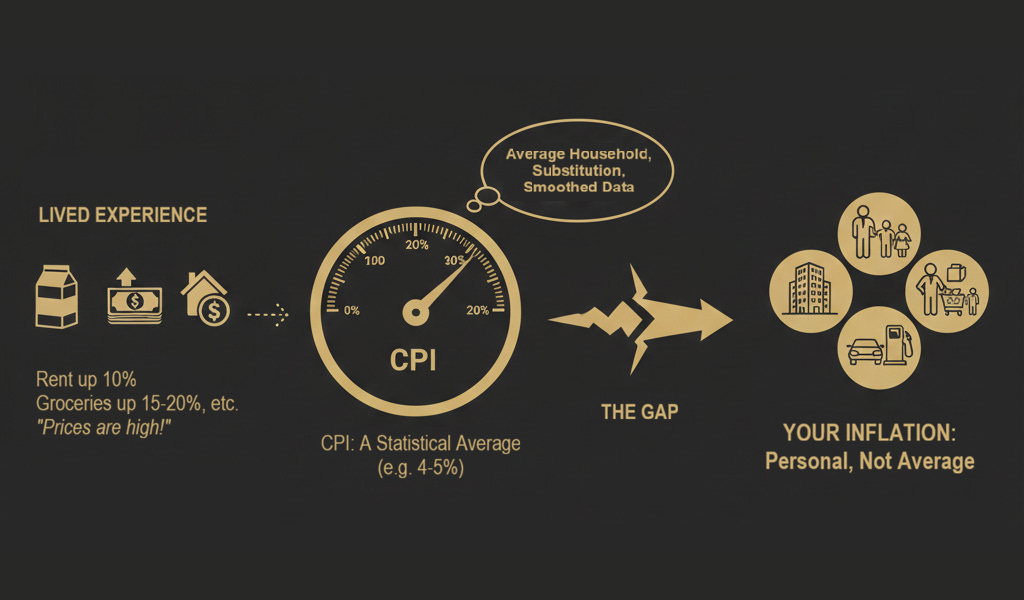

After inflation shows up in daily life, something else usually follows.

Confusion.

You hear that inflation is 4–5%.

But your rent is up 10%.

Your grocery bill feels 15–20% higher.

School fees, healthcare, insurance - none of it seems to match the number.

So a natural conclusion forms:

The inflation number must be wrong.

That conclusion is understandable.

But it isn’t quite accurate.

The problem isn’t that the number is fake.

It’s that the number is answering a different question.

What CPI Is Actually Trying to Measure

The most commonly cited inflation number is CPI - the Consumer Price Index.

At its core, CPI is:

A statistical average

Based on a basket of goods and services

Weighted by how much an “average” household is assumed to consume

That basket includes things like:

Food

Fuel

Housing-related costs

Clothing

Transportation

Some services

Each item has a weight.

Each weight is updated periodically.

Prices are sampled, averaged, smoothed.

From a statistical standpoint, this is not nonsense.

It is a reasonable attempt to summarize a very complex reality.

But that also explains why it often feels disconnected from your life.

Why Your Inflation Rarely Matches CPI

There are three structural reasons CPI rarely feels right at the individual level.

1. CPI Is an Average - You Are Not

CPI describes the experience of a hypothetical average household.

You don’t live in that household.

Your spending depends on:

Your city

Your stage of life

Whether you rent or own

Whether you have children

Whether you rely on services or assets

Two people in the same country can experience wildly different inflation - and both can be correct.

2. CPI Allows Substitution

If the price of one item rises sharply, CPI assumes people substitute toward cheaper alternatives.

Chicken gets expensive → people buy more vegetables.

Brand A rises → people switch to Brand B.

This makes sense statistically.

But it creates a subtle gap emotionally.

CPI asks:

Can you maintain a similar standard of living?

People often feel:

I am being forced to downgrade.

That difference matters.

3. CPI Is Smoothed Over Time

Prices don’t move evenly.

Some jump suddenly.

Some lag.

Some reverse.

CPI smooths these movements to avoid overreacting to short-term noise.

Your life does not.

You experience inflation at the moment of payment, not as a rolling average.

What CPI Does Well - and What It Doesn’t

This is the key distinction.

CPI does a decent job at measuring:

How consumer prices change on average

Over time

For a broad population

CPI does not measure:

Loss of purchasing power for savers

Asset price inflation

Education, healthcare, or housing stress for specific groups

The erosion of money itself

And crucially, CPI does not explain why inflation exists in the first place.

It only describes where it shows up.

Why Governments Rely on CPI

This isn’t about deception.

CPI is useful because:

It is observable

It is repeatable

It is politically and administratively manageable

Governments need a number to:

Adjust pensions

Index wages

Set policy targets

A broad consumer index is practical.

But practicality is not the same as completeness.

Connecting Back to Inflation Itself

In the previous post, we reframed inflation as:

Money buying less.

CPI does not measure that directly.

It measures one downstream effect of that process - consumer prices - filtered through averages, weights, and assumptions.

That’s why CPI can be:

Statistically correct

Conceptually honest

And still feel wrong

All at the same time.

The Takeaway

CPI is not lying to you.

It’s just not talking about you.

It answers:

How are consumer prices changing on average?

Most people are really asking:

Why does my money feel weaker?

Those are related questions - but they are not the same one.

To understand why inflation feels so uneven, we need to look beyond averages and into how inflation distributes itself across people, assets, and income levels.

That’s next.

Disclaimer

This is educational content, not financial, investment, tax, or legal advice.

Zenca shares perspectives and frameworks to help you think clearly - your decisions are your own.

Please think independently and do your own research.

I write to improve how we think about money.

If this helped you think more clearly about money, you can subscribe to Zenca to receive future essays directly.

Every subscription is a vote for thinking more clearly about money.

And if this resonated, take a few seconds to share it — it might change how someone else thinks about money too.