The Cost Of Wanting Things Now (2/4) || EMI vs Investing: What Small Monthly Amounts Add Up To

The same monthly outflow can either disappear - or quietly compound over time.

In the previous piece, we talked about EMIs (equated monthly installments in India) as a patience problem, not a money problem.

Now let’s do something most EMI conversations avoid entirely.

Let’s do the math.

Not complicated math.

Not fancy finance math.

Just honest math.

The ₹1,00,000 (~$1,000) iPhone example

Let’s take a very common purchase.

Price: ₹1,00,000 (~$1,000)

EMI tenure: 24 months

Monthly EMI: roughly ₹4,500 (~$45)

Total outflow after interest: ~₹1,08,000 (~$1,080) (varies by card/bank)

Most people stop here.

“₹4,500 (~$45) a month is manageable.”

And they’re right - monthly it is.

But monthly thinking is exactly where the problem begins.

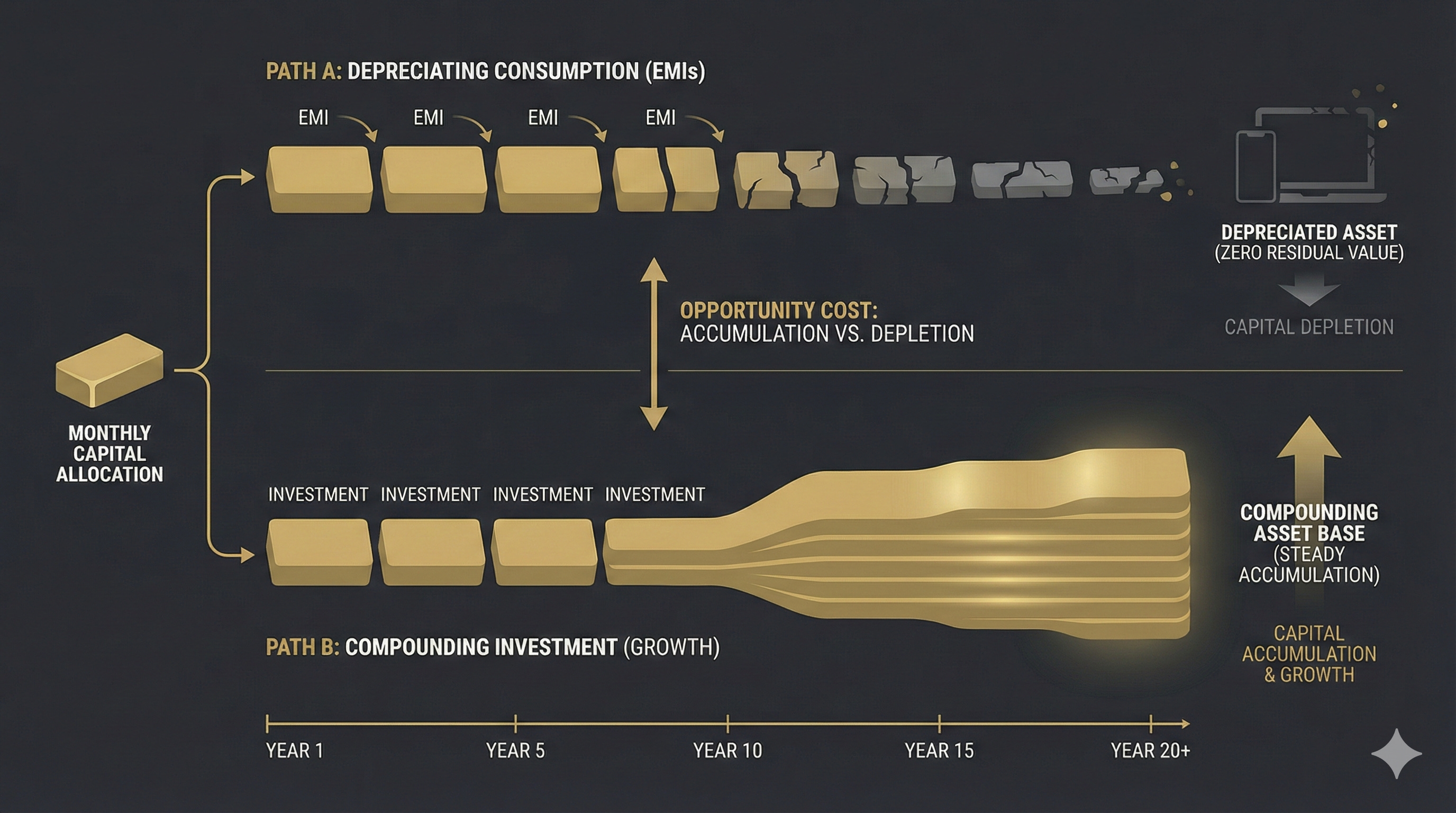

Path 1: Buy now, pay later (the EMI path)

Here’s what actually happens:

You commit ₹4,500/month (~$45/month) for 24 months

You pay interest

You own a phone that starts depreciating the moment you open the box

At the end of 24 months:

The EMI ends

The phone is older

No asset remains

So the visible cost is:

₹1,08,000 (~$1,080) paid for consumption

But that’s only half the story.

Path 2: Delay, invest, then buy (the patience path)

Now let’s look at the alternative most people never consider.

Instead of paying ₹4,500 (~$45) as an EMI, you:

Set aside ₹4,500/month (~$45/month)

Invest it for 24 months

Assume a modest 10% annual return (nothing aggressive)

After 24 months:

Total invested: ₹1,08,000 (~$1,080)

Investment value: ~₹1,23,000 (~$1,230)

Now you have options:

Buy the phone outright

Still have money left

And keep part of your capital working

Same cash outflow.

Radically different outcome.

A fair objection: “But the timelines aren’t the same.”

A reasonable pushback here is:

“If I start an EMI of ₹4,500 (~$45) in January 2026, I get the phone in January 2026.

If I invest ₹4,500 (~$45) starting January 2026, I only get the ₹1,23,000 (~$1,230) corpus in January 2028.

So it’s not the same - the timeline for me getting the phone changes by a full two years.”

That’s true.

And that difference is not a flaw in the comparison.

It is the comparison.

The EMI path gives you the phone immediately and spreads the payment into the future.

The investing path delays the purchase and gives time a chance to work for you.

So the real question isn’t:

“Do both paths give me the phone at the same time?”

It’s:

“What does the same monthly commitment turn into if I change the sequence?”

What actually changed?

Nothing magical.

You didn’t earn more.

You didn’t find a better deal.

You didn’t “optimize” anything.

You just replaced impatience with patience.

And patience quietly did the heavy lifting.

The opportunity cost nobody talks about

When you choose the EMI path, two things happen simultaneously:

You pay interest on consumption

You give up compounding on investment

This second cost is invisible - which is why it’s ignored.

But over a lifetime, this is the cost that matters more.

One EMI doesn’t destroy wealth.

A pattern of EMIs does.

Because every EMI:

Occupies future cash flow

Reduces flexibility

Delays investing

Pushes compounding further away

“But what if I invest after the EMI ends?”

This is the most common justification.

In theory, it sounds reasonable.

In reality:

New EMIs replace old ones

Lifestyle upgrades creep in

Monthly surplus never really shows up

Future discipline is always assumed.

Present impatience is always guaranteed.

This isn’t about never buying things

Let’s be clear again.

This isn’t about:

Never buying a phone

Never using EMIs

Living an ascetic life

It’s about sequence.

Do you consume first and invest later -

or invest first and consume from strength?

That one sequencing decision quietly determines how your financial life unfolds.

The real question to ask before any EMI

Not:

“Can I afford ₹4,500 (~$45) a month?”

But:

“What am I giving up for the next 24 months by locking this cash flow?”

Because money has memory.

And every month you choose consumption over compounding, that choice echoes far longer than the EMI tenure itself.

Next: We’ll break the biggest illusion of all - “zero-cost EMIs” - and explain who really pays when interest supposedly disappears.

Disclaimer

This is educational content, not financial, investment, tax, or legal advice.

Zenca shares perspectives and frameworks to help you think clearly - your decisions are your own.

Please think independently and do your own research.

I write to improve how we think about money.

If this helped you think more clearly about money, you can subscribe to Zenca to receive future essays directly.

Every subscription is a vote for thinking more clearly about money.

And if this resonated, take a few seconds to share it — it might change how someone else thinks about money too.