The Cost Of Wanting Things Now (3/4) || The Truth About “Zero-Cost EMIs”

When interest disappears, cost doesn’t - it just moves out of sight.

“Zero-cost EMI” sounds like a financial miracle.

No interest.

No extra cost.

Same price, just paid over time.

If that were truly the case, it would be the most generous product in modern finance.

It isn’t.

Zero-cost EMIs don’t remove cost.

They just hide it better.

First principles: money always has a cost

Let’s start with a simple rule that never breaks:

If money is used over time, someone pays for that time.

Banks don’t lend for free.

Payment networks don’t operate for free.

Merchants don’t absorb costs out of goodwill.

So when interest appears to disappear, the only real question is:

Who is paying instead of you?

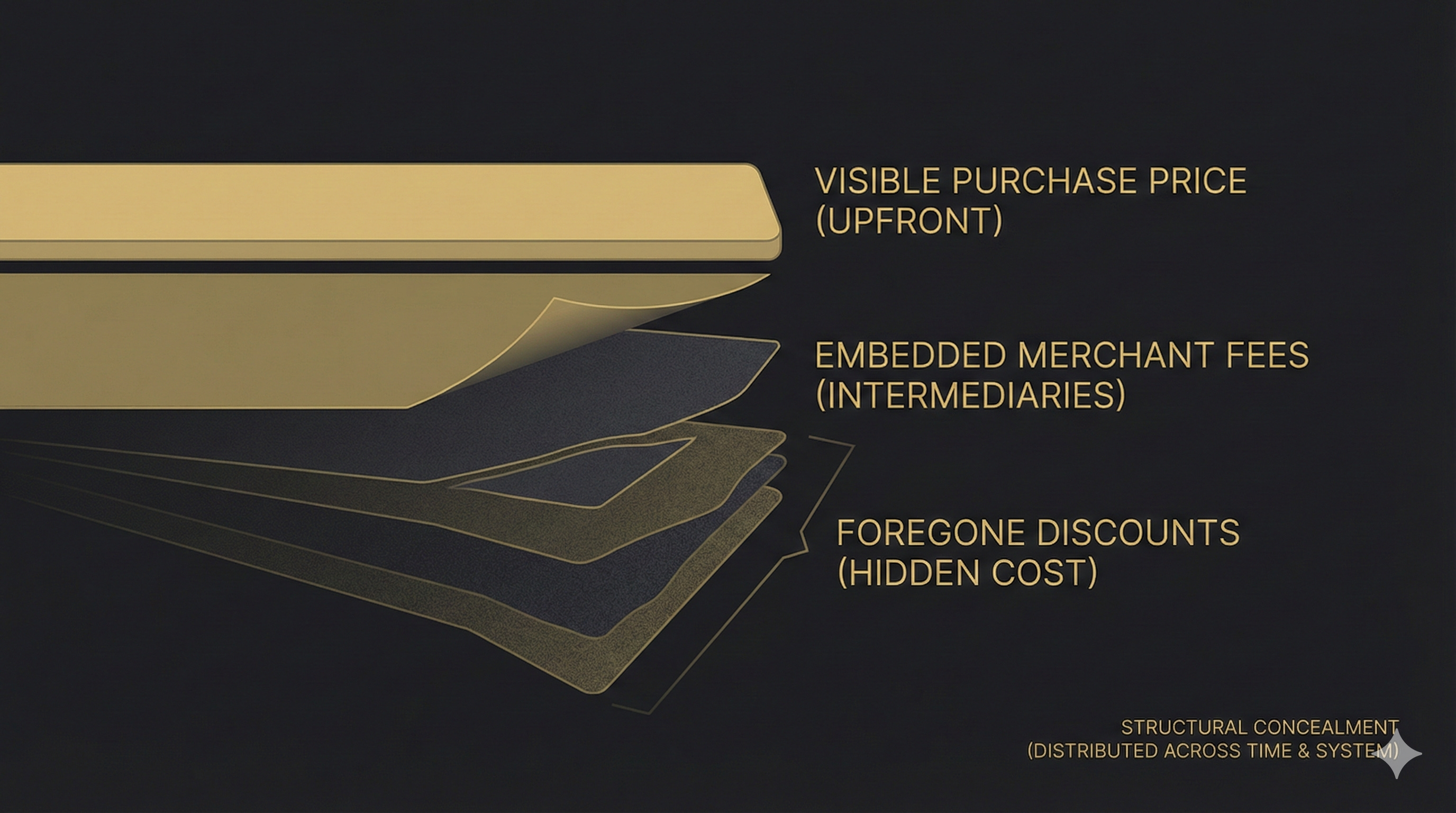

How zero-cost EMIs actually work

Here’s what usually happens behind the scenes.

1. The bank still earns interest

But not from you.

The merchant pays the bank a merchant discount rate (MDR) or a financing fee.

This fee often ranges from 6% to 15%, depending on tenure and card network.

2. The merchant recovers this cost

In one of three ways:

Higher sticker prices

Fewer upfront discounts

Bundled pricing that looks “clean” but isn’t

So while the EMI looks free to you, the cost is baked into the system.

You just don’t see it itemized.

The illusion of “same price”

A common claim is:

“The upfront price and EMI price are the same.”

That comparison is incomplete.

The real comparison is:

Best upfront price with cash

vsZero-cost EMI price

Once you look closely, you’ll often find:

Cash discounts that vanish on EMI

Card-specific pricing that inflates MRPs

Festival “offers” that normalize higher prices

Zero-cost EMIs don’t usually make things cheaper.

They make waiting unnecessary.

What zero-cost EMIs really sell

They don’t sell affordability.

They sell permission.

Permission to:

Buy earlier than you should

Stretch beyond your comfort zone

Commit future income casually

By removing visible interest, zero-cost EMIs neutralize the last psychological barrier people have against debt.

That’s the real product.

Why zero-cost EMIs exist only for consumption

Notice something interesting:

You’ll rarely find:

Zero-cost EMIs for investing

Zero-cost EMIs for productive assets

Zero-cost EMIs for income-generating tools

They exist almost exclusively for:

Phones

Gadgets

Appliances

Lifestyle upgrades

Because zero-cost EMIs are not designed to grow wealth.

They’re designed to accelerate spending.

The opportunity cost still exists

Even if we accept the premise that interest is genuinely zero (which it rarely is), one cost remains unavoidable:

Opportunity cost

Money locked into EMIs:

Can’t be invested

Can’t compound

Can’t create optionality

Zero-cost EMIs remove interest - not impatience.

And impatience still has a price.

The real danger: normalization

The biggest impact of zero-cost EMIs isn’t financial.

It’s behavioral.

They normalize the idea that:

Everything should be bought immediately

Waiting is unnecessary

Monthly payments are harmless

Over time, this shifts how people relate to money:

Cash loses importance

Planning feels optional

Discipline feels outdated

That’s when EMIs stop being tools - and start becoming defaults.

When zero-cost EMIs can make sense

To be fair, there are limited cases where they’re reasonable:

You already have the cash

You’d invest that cash anyway

You’re not using the EMI to stretch affordability

You understand the trade-off clearly

In other words:

The EMI serves you — not your impatience.

That’s a high bar.

Most people don’t clear it.

The question to ask before any zero-cost EMI

Not:

“Is there any interest?”

But:

“If I had to wait and save for this, would I still want it?”

If the answer is no, the problem isn’t the pricing.

It’s the timing.

Next: We’ll go one step further — from structured EMIs to frictionless debt — and unpack how Buy Now, Pay Later quietly rewires spending behavior.

Disclaimer

This is educational content, not financial, investment, tax, or legal advice.

Zenca shares perspectives and frameworks to help you think clearly - your decisions are your own.

Please think independently and do your own research.

I write to improve how we think about money.

If this helped you think more clearly about money, you can subscribe to Zenca to receive future essays directly.

Every subscription is a vote for thinking more clearly about money.

And if this resonated, take a few seconds to share it — it might change how someone else thinks about money too.