The Cost Of Wanting Things Now (4/4) || BNPL: When Impatience Goes Instant

When friction disappears, reflection goes with it - but obligations don’t.

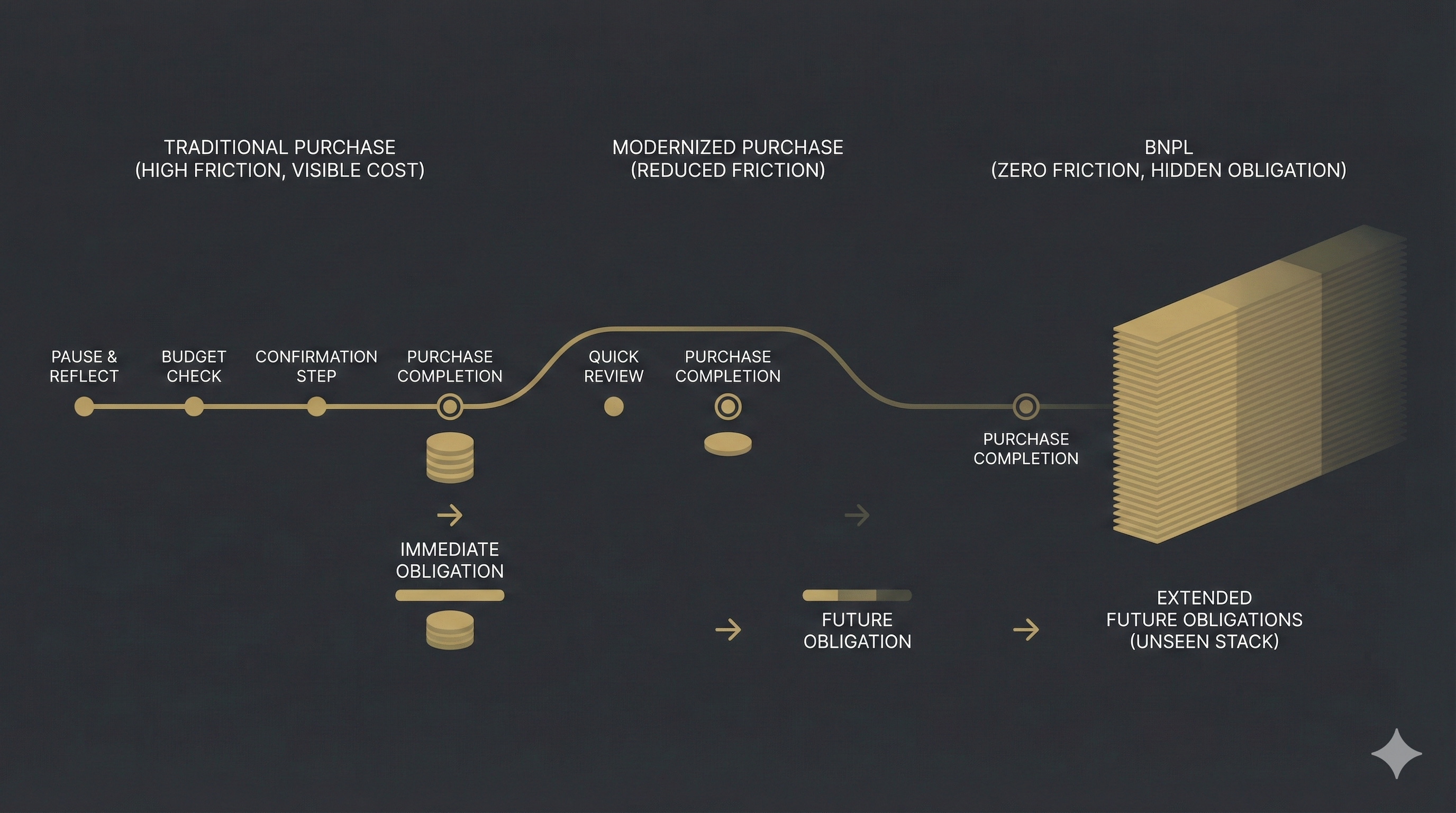

EMIs at least make you pause.

There’s paperwork.

A bank.

A tenure.

A monthly reminder that you owe money.

Buy Now, Pay Later removes all of that.

No friction.

No reflection.

No discomfort.

Just a button.

That’s not innovation.

That’s impatience, fully automated.

What BNPL really changes

BNPL doesn’t change what you buy.

It changes when you feel the cost.

Traditional payments make you feel pain before consumption.

EMIs move pain after consumption.

BNPL tries to remove pain altogether.

But pain doesn’t disappear.

It accumulates.

Why BNPL feels harmless

BNPL works because it hijacks three powerful biases:

1. The amounts are “too small to matter”

₹1,200 (~$12) here.

₹2,800 (~$28) there.

₹900 (~$9) somewhere else.

Individually insignificant.

Collectively dangerous.

2. The payment is deferred, not denied

You’re not saying no.

You’re saying:

“I’ll deal with this later.”

Later is always more accommodating than today.

3. There’s no visible debt signal

No credit card statement.

No EMI schedule.

No sense of obligation.

Just usage.

That’s the trick.

From structured debt to invisible debt

EMIs are formal.

They:

Have tenures

Force monthly discipline

Show up clearly in budgets

BNPL is informal.

It:

Spreads across apps

Avoids central visibility

Encourages stacking

You don’t feel indebted.

You just feel slightly poorer every month.

Why BNPL targets younger earners

BNPL is not designed for people with surplus.

It’s designed for people with:

Early income

Rising aspirations

Limited buffers

High social pressure

People who are still building patience as a muscle.

That’s not accidental.

It’s the business model.

The real danger isn’t default - it’s habit

Most BNPL users don’t default.

That’s not the problem.

The problem is behavioral training.

BNPL trains you to:

Prioritize desire over planning

Detach consumption from consequence

Treat future income as already spent

Once that wiring sets in, it leaks into bigger decisions:

Credit cards

Personal loans

Lifestyle inflation

Long-term financial fragility

Why BNPL never creates assets

Notice the pattern again.

BNPL is rarely used for:

Education

Skill-building

Productive tools

Long-term value creation

It’s used for:

Fashion

Gadgets

Convenience

Impulse upgrades

BNPL doesn’t finance growth.

It finances urgency.

“But I pay it off on time”

Most users say this.

And most are telling the truth.

But punctual repayment isn’t the same as financial health.

You can:

Pay everything on time

Have no overdue bills

Still quietly sabotage wealth creation

Because every BNPL payment:

Crowds out investing

Reduces slack

Steals optionality

Just without drama.

The common thread across EMIs, zero-cost EMIs, and BNPL

Different products.

Same principle.

They reduce waiting.

And waiting is not a nuisance.

Waiting is where:

Priorities clarify

Wants fade

Better decisions emerge

When waiting disappears, judgment follows.

The discipline BNPL removes

BNPL doesn’t just remove friction.

It removes self-interrogation.

That moment where you ask:

“Do I really need this?”

That moment matters more than any interest rate ever will.

The only question that matters

Before any BNPL purchase, ask:

“If I had to pay for this today, would I still buy it?”

If the answer is no, the problem isn’t the payment option.

It’s impatience wearing better UX.

Wealth is built slowly - by design

There is no shortcut around patience.

You can delay it.

You can disguise it.

You can finance around it.

But eventually, wealth only responds to one thing:

The ability to say not now - long enough.

BNPL doesn’t make things affordable.

It makes restraint optional.

And restraint is the real asset.

Closing note (series wrap)

EMIs.

Zero-cost EMIs.

BNPL.

Three products.

One trade-off.

Patience or impatience.

One compounds quietly.

The other compounds invisibly.

Choose carefully.

Disclaimer

This is educational content, not financial, investment, tax, or legal advice.

Zenca shares perspectives and frameworks to help you think clearly - your decisions are your own.

Please think independently and do your own research.

I write to improve how we think about money.

If this helped you think more clearly about money, you can subscribe to Zenca to receive future essays directly.

Every subscription is a vote for thinking more clearly about money.

And if this resonated, take a few seconds to share it — it might change how someone else thinks about money too.