Decision-Making Under Uncertainty (1/3) || You Can’t Have High Returns, Short Time, And Low Risk

Why “safe 20% annualized returns in five years” is an impossible ask

This article is part of the Zenca series Decision-Making Under Uncertainty, which explores how to make better financial choices when outcomes cannot be predicted.

Most financial mistakes don’t come from ignorance.

They come from asking for combinations that cannot exist.

When you strip away product names, advisors, stories, and market noise, almost everyone is asking for the same thing:

“I want returns higher than FDs (fixed deposits in India), within about five years, with very high certainty.”

It sounds reasonable.

It sounds mature.

It even sounds conservative.

But it isn’t.

Because that requirement contains a contradiction that markets cannot resolve.

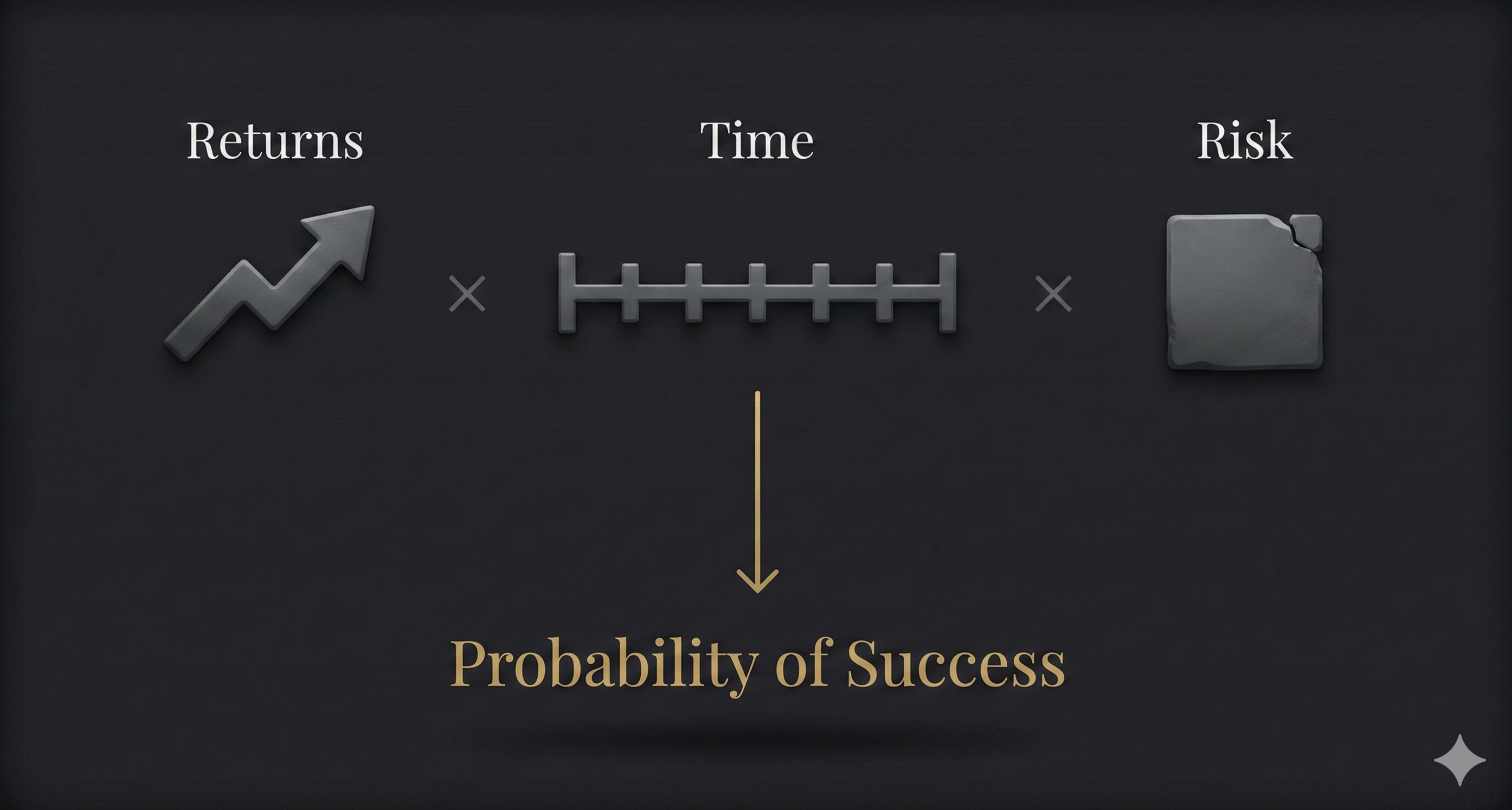

The canonical trade-off

Here is the only framework worth remembering:

Returns × Time × Risk → Probability of Success

Returns, Time, and Risk (to corpus) are the inputs you choose.

Probability of success is the output you get.

“Certainty” is not a dimension.

It’s a feeling people want - and markets don’t hand out feelings for free.

Once you see decisions through this lens, most “confusion” disappears.

What remains is just trade-offs.

Why this combination breaks

Let’s restate the expectation cleanly.

What most people are effectively trying to lock at the same time is:

High returns

Short time

Low risk to corpus

…and therefore a high probability of success

Is this possible?

Theoretically: Yes

Structurally: No

Probabilistically: No

Repeatably: No

Markets allow any two of these.

Never all three.

Risk, properly defined

Higher returns always come with higher risk.

Not sometimes.

Not usually.

Not depending on the product.

Always.

But we need to be precise about what “risk” actually means here.

Risk is risk to corpus.

It is the possibility that the capital itself goes down or is impaired.

That is the only risk that truly changes your future.

Where many people get this wrong is in how they think about failure when chasing high returns.

When someone picks individual stocks or invests through a PMS with an expectation of, say, 20% returns, they often carry an implicit assumption:

“If I don’t get 20%, I’ll at least get 15%.”

That assumption is an illusion.

The risk in chasing 20% returns is not that you might end up with slightly lower returns than promised.

The risk is that the very reason 20% returns are possible is because capital loss is also possible.

If capital loss were not on the table, 20% returns could not exist in the first place.

So when a high-return strategy fails, you don’t get to choose a softer landing.

What failure often looks like in practice

You start with 100 units.

A portion of the portfolio suffers meaningful loss:

20 units fall by 40% → –8

Other parts do reasonably well:

20 units grow by 10% → +2

20 units grow by 20% → +4

20 units grow by 30% → +6

20 units grow by 40% → +8

Add it all up:

100 units → 112 units

Net return: ~12%

On paper, there were stocks that did 30% and 40%.

In reality, capital impairment elsewhere pulled the entire outcome down.

This is the part most people miss.

They focus on the winners.

They forget that losses don’t just subtract returns - they shrink the base on which all future returns compound.

Once capital is impaired:

recovery time increases non-linearly

probability of success drops sharply

and future options narrow

Volatility, uncertainty, and noise matter only because they increase the chance of this happening - either directly, or by forcing decisions that lock in losses.

That is what “risk” really means.

Why “5 years” keeps showing up (this matters)

The five-year time horizon is not a financial construct.

It’s a psychological one.

People don’t arrive at five years by studying market cycles or return distributions.

They arrive at it because five years feels:

long enough to wait,

but short enough to stay emotionally engaged.

In reality, five years is:

short in markets,

long in human patience

This is where the expectation breaks.

Five years feels responsible.

Twenty percent feels ambitious but not crazy.

Near certainty feels like prudence.

Individually, each sounds reasonable.

Together, they form an impossible requirement.

The three common paths (the framework in real life)

Here are three common “paths” people take.

These are not product recommendations.

They are just different combinations of Returns, Time, and Risk to corpus - which then imply different probabilities of success.

With FDs, you buy certainty by selling time.

With equity ETFs, you accept volatility to buy back years of life.

With concentrated bets (PMS (portfolio management services in India), or stock picking, or using leverage), you are betting on being exceptional.

Some are. Most aren’t.

Probability of success is the outcome, not the choice

This is where the confusion usually comes from.

People talk as if they are choosing “certainty” directly.

They aren’t.

You don’t pick probability of success off a menu.

You imply it.

Probability of success is what you get after you choose:

how high your return target is

how short your time horizon is

how much risk to corpus you are willing to tolerate

The objective, for any rational actor, should be simple:

choose a combination of Returns, Time, and Risk that maximises your probability of success - ideally as close to 100% as possible, or at least close enough that you can live with it.

Once probability drops meaningfully, you are no longer investing - you are speculating.

Anything around 50% is no better than a coin flip.

Anything below that is indistinguishable from gambling.

That doesn’t mean such choices are always wrong.

It does mean they should be recognised for what they are - deliberate bets, not robust plans.

This is why “certainty” feels so slippery in investing: it isn’t a standalone variable.

It’s the result of the variables you already chose.

The least destructive adjustment

If higher-than-FD returns are the goal, something in this expectation has to give.

The question is not whether to compromise.

It is where to do so with the least long-term damage.

In most cases, the least destructive adjustment is to relax the need to lock everything down - not by being vague, but by being precise about what you are actually relaxing.

What usually has to flex is:

Time (it may take longer than five years), and/or

Return precision (it may not be twenty percent)

What is far more expensive to “relax” is risk to corpus.

Once once capital is impaired, recovery becomes nonlinear - and often permanent.

In other words, it is usually better to accept that results may take longer, or look different than expected, than to accept a strategy that risks knocking you out of the game entirely.

The honest conclusion

There is no “best” investment.

There is only:

the return you want

the time you have

the risk to corpus you are willing to take

Ignore that trade-off, and the market will enforce it for you - usually when you least want it to.

One line to remember

High returns, short time, and low risk cannot coexist.

Choose the two you value most — and accept the cost of the third.

Once you see this trade-off clearly, the question changes.

It stops being “How do I get these returns?”

And becomes “Given uncertainty, which variables am I actually willing to live with?”

That question - not returns - is where better decisions begin.

In the next piece, I’ll explain how I personally answer it, and why I choose to optimise for probability of success rather than chasing returns.

Disclaimer

This is educational content, not financial, investment, tax, or legal advice.

Zenca shares perspectives and frameworks to help you think clearly - your decisions are your own.

Please think independently and do your own research.

I write to improve how we think about money.

If this helped you think more clearly about money, you can subscribe to Zenca to receive future essays directly.

Every subscription is a vote for thinking more clearly about money.

And if this resonated, take a few seconds to share it — it might change how someone else thinks about money too.